ING’s Chris Turner reports that the Reserve Bank of Australia kept rates at 4.35%, while Governor Michele Bullock delivered a hawkish message, stressing upside inflation risks and revealing that a hike was discussed. Short-dated Australian yields reversed higher. ING’s FX team does not expect further RBA hikes this year but still projects AUD/USD rising toward 0.73 by year-end.

Hawkish RBA and AUD/USD upside

"The Reserve Bank of Australia left rates unchanged at 4.35% today. Some argue that the added description of the policy as 'somewhat restrictive' means that the RBA is less likely to hike in future."

"However, Governor Michele Bullock proved quite hawkish at the press conference, reminding the audience that the RBA sees inflation risks as skewed to the upside and admitting that the RBA did discuss the possibility of a rate hike at today's meeting."

"Our team does not see a further RBA rate hike this year, but from an FX perspective, we still see AUD/USD heading up to 0.73 by year-end."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

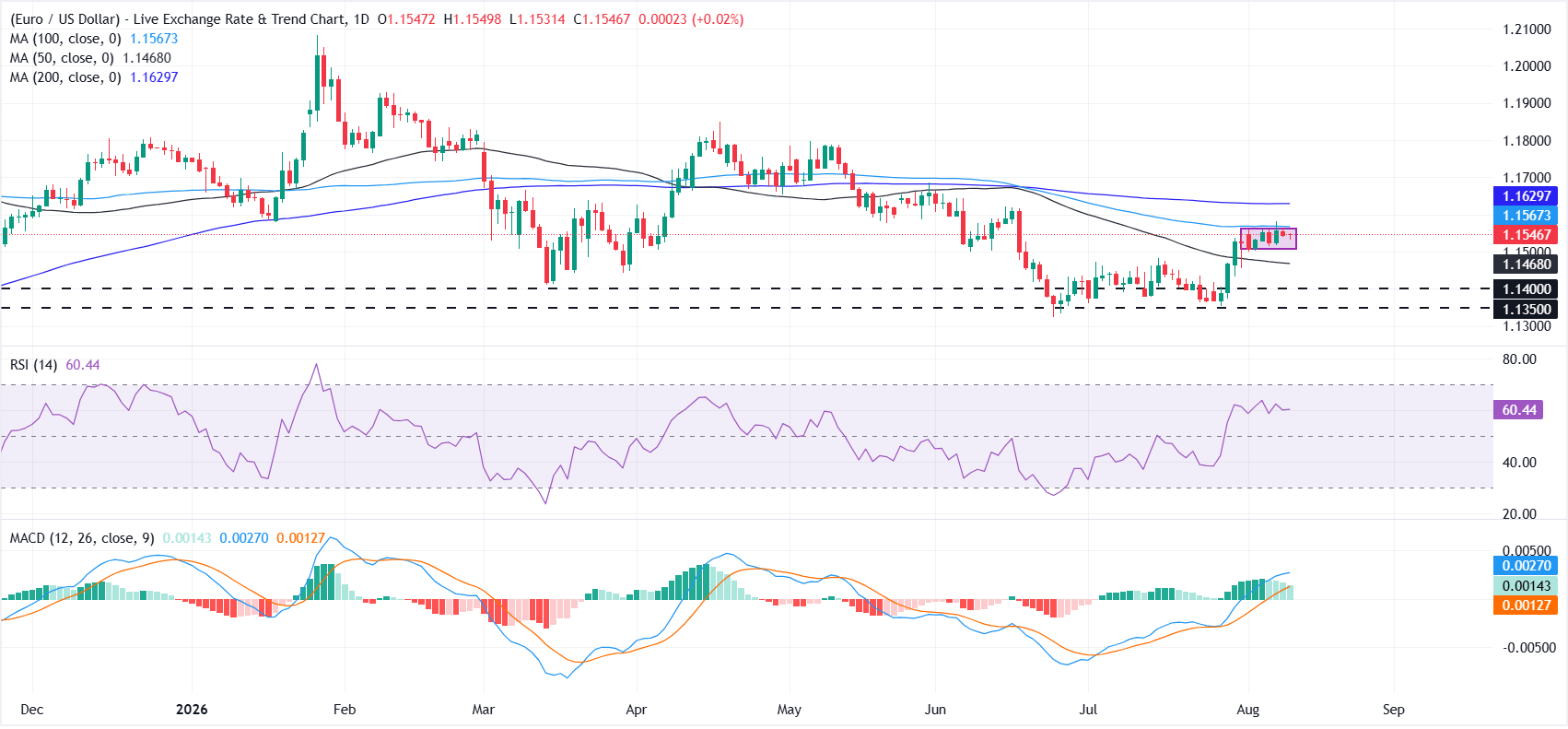

- EUR/USD remains range-bound as the 100-day SMA keeps buyers in check.

- RSI and MACD readings point to a mild bullish bias despite the sideways price action.

- A break above the 100-day SMA would bring the 200-day SMA into focus.

EUR/USD fluctuates on Tuesday, holding within the range seen over the past week. At the time of writing, the pair trades around 1.1546, virtually unchanged on the day.

The sideways price action comes as the US Dollar (USD) stabilizes near its recent lows, with traders closely monitoring developments in the Middle East, particularly around the reopening of the Strait of Hormuz.

Attention also turns to Wednesday’s US Consumer Price Index (CPI) data, which could shape Federal Reserve (Fed) rate expectations for the September meeting and drive the next move in the US Dollar and, in turn, EUR/USD.

Euro seen grinding higher as Fed independence erodes and Dollar overvaluation unwinds

According to Commerzbank, the EUR/USD exchange rate is likely to regain traction once geopolitical tensions ease, with the bank arguing that "the EUR/USD exchange rate should rise again after the war ends and continue to drift higher in the following quarters due to the eroding independence of the U.S. Federal Reserve, especially since the dollar is significantly overvalued in terms of purchasing power parity." The bank also highlights the policy-rate backdrop, stating that "we expect US interest rate expectations to correct even further downward in the coming months, weighing on the dollar."

Reflecting these factors, the bank has trimmed but maintained a constructive medium‑term profile for the pair, now projecting that “we expect the EUR/USD rate to be 1.18 by mid-2027 (previously 1.20)” and, “all in all, we expect a gradual rise in EUR-USD toward 1.19 by the end of 2027 (previous forecast: 1.21).”

Technical analysis: Daily chart

EUR/USD is hovering between the short- and longer-term moving averages and thus maintaining a neutral near-term bias. Momentum remains constructive, with the Relative Strength Index (RSI) on the daily chart near 59 hinting at persistent buying interest and the Moving Average Convergence Divergence (MACD) line in positive territory, suggesting a mild bullish tone in the backdrop despite the layered resistance above price.

On the downside, initial support is seen at the 50-day SMA at 1.1468, followed by a horizontal floor at 1.1400 and a deeper structural base near 1.1350.

On the topside, immediate resistance is located at the 100-day SMA at 1.1567, with a more significant barrier at the 200-day SMA at 1.1630. A sustained break above these levels would be needed to unlock a more convincing bullish phase, while failure to do so would keep the pair confined within its current range.

(The technical analysis of this story was written with the help of an AI tool. Know more.)

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the British Pound.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.02% | 0.02% | -0.06% | -0.02% | -0.22% | -0.08% | -0.02% | |

| EUR | 0.02% | 0.04% | -0.04% | 0.01% | -0.16% | -0.06% | 0.00% | |

| GBP | -0.02% | -0.04% | -0.09% | -0.04% | -0.21% | -0.10% | -0.04% | |

| JPY | 0.06% | 0.04% | 0.09% | 0.05% | -0.14% | -0.02% | 0.06% | |

| CAD | 0.02% | -0.01% | 0.04% | -0.05% | -0.18% | -0.07% | -0.00% | |

| AUD | 0.22% | 0.16% | 0.21% | 0.14% | 0.18% | 0.11% | 0.18% | |

| NZD | 0.08% | 0.06% | 0.10% | 0.02% | 0.07% | -0.11% | 0.07% | |

| CHF | 0.02% | -0.01% | 0.04% | -0.06% | 0.00% | -0.18% | -0.07% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

Commerzbank’s Carsten Fritsch notes Gold breaking above USD 4,400 per ounce despite a sharp Oil rally, with Fed rate expectations only modestly higher after weak US labour data. ETF investors added 14.5 tons over four days, and global Gold ETFs saw July inflows of 23.5 tons, mainly in Europe and Asia. Fritsch remains sceptical that Gold can defy higher Oil and rates for long.

Price surge driven by ETF demand

"This morning, the gold price rose above the USD 4,400 per troy ounce mark for the first time since early June."

"Despite the higher oil price, interest rate expectations have risen only slightly and remain lower than they were before Friday’s disappointing US labour market data."

"Gold is receiving a boost from ETF investors."

"According to data from Bloomberg, there have been inflows into gold ETFs totalling 14.5 tons over the last four trading days."

"We view the recent price rise with scepticism, as interest rate expectations are unlikely to decouple from higher oil prices on a sustained basis."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

Rabobank's Senior FX Strategist Jane Foley examines Japanese inflation dynamics and Bank of Japan policy. The report notes elevated Oil prices and supply risks, but stresses BoJ’s focus on core inflation and wage-driven pressures after decades of deflation. It highlights BoJ’s warning that core CPI could exceed 2%, raising prospects of a rate hike around September or October.

Core CPI, wage growth and BoJ outlook

"While a loosening in the labour market reduces the chances of second order price effects, elevated oil prices may still push various G10 central banks into more hawkish policy positions this year. Not only does the continued (near) closure of the Strait of Hormuz imply inflationary risks for the Fed, but it may also raise the prospect of the USD finding fresh safe haven support. This scenario would clearly be far from optimal for the MoF."

"However, the BoJ has been focussed on core inflation and ensuring there has been a sufficient psychology change within firms to move away from cost cutting behaviour in favour of wage hikes. In its latest Outlook for Economic Activity and Prices the BoJ has flagged the risk that core CPI could deviate above the 2% inflation target. This raises the prospect of a September rate hike from the BoJ, but for now the market is focussing on the potential for an October move."

"More signs of resilience in the Japanese economy and an uplift in growth expectations would help reduce fiscal concerns. As it stands, however, the government will likely have to make more effort to respond to the market’s concerns about fiscal discipline in order to reassure investors and calm the JPY."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

DBS Group Research economist Chua Han Teng highlights that Singapore’s economy is set to deliver above-trend growth for a third straight year in 2026, supported by manufacturing, wholesale trade and financial services. Following a robust 2Q26 performance and the ongoing global AI boom, DBS raises its 2026 real GDP growth forecast to 5.0%, noting MTI’s upgraded official projection and lingering geopolitical challenges.

Above-trend expansion driven by AI

"Singapore’s economic growth was robust in 2Q26, as confirmed by the Ministry of Trade and Industry (MTI). GDP growth was revised up to 5.9% yoy and 1.4% qoq sa, in line with our expectations."

"The modest upward revision from the advance estimates of 5.7% yoy and 1.1% qoq sa reflected firmer expansion in the manufacturing and services sectors. Growth was driven by the strong performance of manufacturing, wholesale trade, and finance & insurance sectors."

"We are raising our 2026 GDP growth forecast to 5.0%, from 4.3%, on the back of strong 1H26 performance, and the likely persistence of the global artificial intelligence (AI) boom."

"This is despite ongoing geopolitical challenges, and a moderation in the overall GDP cycle due partly to high base effects."

"MTI also further upgraded its official 2026 GDP growth projection to 4.5%-5.5%, from 2.0-4.0%, considering the improved external demand outlook, despite continuing to acknowledge downside risks to the global economy."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

Chris Turner at ING observes that EUR/USD realised volatility continues to decline, with one-year volatility matching lows from November 2024. He argues this calm backdrop is unlikely to change before mid-September, and warns that underhedged European investors in US assets may need to raise Dollar hedge ratios if the Dollar weakens. EUR/USD is expected to stay within 1.1515-1.1560 today.

Calm trading and hedge ratio risks

"EUR/USD realised volatility continues to sink and one-year is now at 5.8% – matching the low from November 2024. As above, it is hard to see that environment changing anytime soon – or at least until mid-September when central bankers around the world return from their summer breaks."

"We published an article yesterday looking at the dollar hedge ratios of European investors. The risk here is that European investors in the US are once again underhedged and have to quickly raise their dollar hedge ratios should the dollar look vulnerable again."

"It is hard to see EUR/USD trading much outside a 1.1515-1.1560 range today."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

Volkmar Baur at Commerzbank notes that the Japanese Yen has weakened again above 159 per Dollar despite recent intervention and Bank of Japan signals. He argues JPY is fundamentally too weak, with strong current account and credit data, but rising Japanese equities and associated hedge adjustments may keep JPY under pressure until the Bank of Japan clarifies its rate-hike plans.

Fundamentals strong but pressure persists

"Speaking of intervention, the Japanese yen rose above 159 against the U.S. dollar again yesterday, indicating that it has weakened once more in recent days. This was to be expected."

"Following the Bank of Japan’s meeting, we had already noted that the Bank of Japan would need to send clearer signals that it is considering raising interest rates more quickly than it has so far."

"Governor Ueda did give subtle signals during his press conference. And the “summary of opinions” released yesterday also contains indications that the bank could raise interest rates more quickly. However, the market still seems to find this somewhat insufficient."

"According to a survey by the Japan Exchange Group, around 35% of Japanese stocks are now held by foreign investors. Since these Japanese stocks are largely held in currency-hedged positions, rising stock prices (the Nikkei is up 35% this year) require corresponding adjustments to currency hedges, which tends to weigh on the JPY."

"While this is likely not the main reason, it could also contribute to the JPY coming under pressure again in the coming weeks until the Bank of Japan clarifies its plans more clearly."

"We remain convinced that the Japanese yen is currently trading too weakly and should be somewhat stronger on a fundamental basis. This was evident again yesterday in robust figures for the current account and credit growth. At the same time, days like yesterday show that rising stock prices can contribute to a weakening of the currency."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

- USD/JPY holds steady as a firmer US Dollar and elevated Oil prices weigh on the Japanese Yen.

- The Yen struggles to build on recent intervention-driven gains despite signs that the BoJ could raise rates again in September.

- Traders await US CPI data for fresh clues on the Fed’s next move.

USD/JPY treads water on Tuesday as the Japanese Yen (JPY) struggles to find its footing, facing headwinds from a firmer US Dollar (USD) and elevated Oil prices. At the time of writing, the pair trades around 159.24 after hitting an intraday low of 158.92.

Rabobank’s strategists observe that “the joint Japanese-US intervention in the JPY exchange rate is starting to lose its grip on the currency.” While “the prospect of further FX interventions continues to provide some support,” they point out that “USD/JPY is gradually drifting higher, and the currency has reversed about half of the peak-to-trough move versus both EUR and USD.”

Plans to reopen the Strait of Hormuz remain uncertain, even as talks between Iran and Oman have moved to an advanced stage, according to Qatar’s Foreign Ministry spokesperson. Earlier, Iran outlined several demands from the US, including lifting sanctions, releasing frozen Iranian assets, ending military threats and removing the naval blockade.

Higher Oil prices are raising concerns about the inflation outlook and supporting expectations that the Federal Reserve (Fed) may need to raise interest rates. The CME FedWatch tool shows a 51.9% chance of a rate hike at the September meeting.

Hawkish Fed expectations and geopolitical tensions are helping the US Dollar hold near its recent lows. The US Dollar Index (DXY), which tracks the Greenback's value against six major currencies, trades around 99.85.

On the data front, the ADP Employment Change four-week average fell to 8.25K from a downwardly revised 11K. Traders now await Wednesday’s US Consumer Price Index (CPI) data.

Meanwhile, elevated Oil prices are likely to keep the Japanese Yen under pressure in the near term, given Japan’s heavy dependence on imported energy.

Rabobank reiterates that “these FX interventions may prop up the currency temporarily, but it will probably not last unless there are structural improvements in the yen’s fundamentals,” adding that “the government’s plans are unlikely to do this in the near-term.”

In addition, Rabobank highlights that “interest rate differentials are also weighing on the currency,” even as the BoJ begins to signal a willingness to address this. The bank notes that “sources within the Bank of Japan told reporters that policymakers could raise rates again in September,” comments which “follow a relatively hawkish write-up of the July meeting.”

Japanese Yen Price Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the British Pound.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.06% | 0.09% | -0.03% | -0.00% | -0.14% | 0.07% | 0.01% | |

| EUR | -0.06% | 0.04% | -0.07% | -0.04% | -0.16% | 0.02% | -0.04% | |

| GBP | -0.09% | -0.04% | -0.11% | -0.06% | -0.20% | -0.03% | -0.07% | |

| JPY | 0.03% | 0.07% | 0.11% | 0.03% | -0.10% | 0.09% | 0.04% | |

| CAD | 0.00% | 0.04% | 0.06% | -0.03% | -0.11% | 0.07% | 0.00% | |

| AUD | 0.14% | 0.16% | 0.20% | 0.10% | 0.11% | 0.18% | 0.12% | |

| NZD | -0.07% | -0.02% | 0.03% | -0.09% | -0.07% | -0.18% | -0.05% | |

| CHF | -0.01% | 0.04% | 0.07% | -0.04% | -0.01% | -0.12% | 0.05% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

- US private employers added an average of 8.25K jobs per week in late July.

- Job gains lose further momentum, adding to the previous week’s pullback.

Private-sector hiring in the US has further cooled in late July. According to the NER Pulse, the weekly companion to the ADP National Employment Report, companies added an average of 8.25K jobs per week in the four weeks ending July 25.

That marks another pullback from the prior reading (11K), showing an extra impasse in hiring.

Market reaction

The Greenback clings to its daily gains, building on Monday’s uptick and prompting the US Dollar Index (DXY) to trade just below the psychological 100.00 barrier.

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.