Volkmar Baur at Commerzbank notes that the Japanese Yen has weakened again above 159 per Dollar despite recent intervention and Bank of Japan signals. He argues JPY is fundamentally too weak, with strong current account and credit data, but rising Japanese equities and associated hedge adjustments may keep JPY under pressure until the Bank of Japan clarifies its rate-hike plans.

Fundamentals strong but pressure persists

"Speaking of intervention, the Japanese yen rose above 159 against the U.S. dollar again yesterday, indicating that it has weakened once more in recent days. This was to be expected."

"Following the Bank of Japan’s meeting, we had already noted that the Bank of Japan would need to send clearer signals that it is considering raising interest rates more quickly than it has so far."

"Governor Ueda did give subtle signals during his press conference. And the “summary of opinions” released yesterday also contains indications that the bank could raise interest rates more quickly. However, the market still seems to find this somewhat insufficient."

"According to a survey by the Japan Exchange Group, around 35% of Japanese stocks are now held by foreign investors. Since these Japanese stocks are largely held in currency-hedged positions, rising stock prices (the Nikkei is up 35% this year) require corresponding adjustments to currency hedges, which tends to weigh on the JPY."

"While this is likely not the main reason, it could also contribute to the JPY coming under pressure again in the coming weeks until the Bank of Japan clarifies its plans more clearly."

"We remain convinced that the Japanese yen is currently trading too weakly and should be somewhat stronger on a fundamental basis. This was evident again yesterday in robust figures for the current account and credit growth. At the same time, days like yesterday show that rising stock prices can contribute to a weakening of the currency."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

- USD/JPY holds steady as a firmer US Dollar and elevated Oil prices weigh on the Japanese Yen.

- The Yen struggles to build on recent intervention-driven gains despite signs that the BoJ could raise rates again in September.

- Traders await US CPI data for fresh clues on the Fed’s next move.

USD/JPY treads water on Tuesday as the Japanese Yen (JPY) struggles to find its footing, facing headwinds from a firmer US Dollar (USD) and elevated Oil prices. At the time of writing, the pair trades around 159.24 after hitting an intraday low of 158.92.

Rabobank’s strategists observe that “the joint Japanese-US intervention in the JPY exchange rate is starting to lose its grip on the currency.” While “the prospect of further FX interventions continues to provide some support,” they point out that “USD/JPY is gradually drifting higher, and the currency has reversed about half of the peak-to-trough move versus both EUR and USD.”

Plans to reopen the Strait of Hormuz remain uncertain, even as talks between Iran and Oman have moved to an advanced stage, according to Qatar’s Foreign Ministry spokesperson. Earlier, Iran outlined several demands from the US, including lifting sanctions, releasing frozen Iranian assets, ending military threats and removing the naval blockade.

Higher Oil prices are raising concerns about the inflation outlook and supporting expectations that the Federal Reserve (Fed) may need to raise interest rates. The CME FedWatch tool shows a 51.9% chance of a rate hike at the September meeting.

Hawkish Fed expectations and geopolitical tensions are helping the US Dollar hold near its recent lows. The US Dollar Index (DXY), which tracks the Greenback's value against six major currencies, trades around 99.85.

On the data front, the ADP Employment Change four-week average fell to 8.25K from a downwardly revised 11K. Traders now await Wednesday’s US Consumer Price Index (CPI) data.

Meanwhile, elevated Oil prices are likely to keep the Japanese Yen under pressure in the near term, given Japan’s heavy dependence on imported energy.

Rabobank reiterates that “these FX interventions may prop up the currency temporarily, but it will probably not last unless there are structural improvements in the yen’s fundamentals,” adding that “the government’s plans are unlikely to do this in the near-term.”

In addition, Rabobank highlights that “interest rate differentials are also weighing on the currency,” even as the BoJ begins to signal a willingness to address this. The bank notes that “sources within the Bank of Japan told reporters that policymakers could raise rates again in September,” comments which “follow a relatively hawkish write-up of the July meeting.”

Japanese Yen Price Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the British Pound.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.06% | 0.09% | -0.03% | -0.00% | -0.14% | 0.07% | 0.01% | |

| EUR | -0.06% | 0.04% | -0.07% | -0.04% | -0.16% | 0.02% | -0.04% | |

| GBP | -0.09% | -0.04% | -0.11% | -0.06% | -0.20% | -0.03% | -0.07% | |

| JPY | 0.03% | 0.07% | 0.11% | 0.03% | -0.10% | 0.09% | 0.04% | |

| CAD | 0.00% | 0.04% | 0.06% | -0.03% | -0.11% | 0.07% | 0.00% | |

| AUD | 0.14% | 0.16% | 0.20% | 0.10% | 0.11% | 0.18% | 0.12% | |

| NZD | -0.07% | -0.02% | 0.03% | -0.09% | -0.07% | -0.18% | -0.05% | |

| CHF | -0.01% | 0.04% | 0.07% | -0.04% | -0.01% | -0.12% | 0.05% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

- US private employers added an average of 8.25K jobs per week in late July.

- Job gains lose further momentum, adding to the previous week’s pullback.

Private-sector hiring in the US has further cooled in late July. According to the NER Pulse, the weekly companion to the ADP National Employment Report, companies added an average of 8.25K jobs per week in the four weeks ending July 25.

That marks another pullback from the prior reading (11K), showing an extra impasse in hiring.

Market reaction

The Greenback clings to its daily gains, building on Monday’s uptick and prompting the US Dollar Index (DXY) to trade just below the psychological 100.00 barrier.

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.

Brown Brothers Harriman’s (BBH) Elias Haddad reports the Reserve Bank of Australia (RBA) delivered a less hawkish hold, keeping rates at 4.35% and judging policy “somewhat restrictive” as the labor market has eased more than expected. Haddad notes the RBA softened its hawkish bias, raised the bar for further hikes, and saw AUD/USD briefly dip before recovering during Governor Bullock’s press conference.

Carry and commodities support Aussie

"RBA delivered a less hawkish hold. As was widely expected, the RBA kept the policy rate at 4.35% for a second straight meeting. The decision was unanimous, with the Board judging policy to be “somewhat restrictive” and noting that “labour market conditions have eased by a little more than expected in recent months.”"

"The RBA softened its hawkish bias. It reiterated that “inflation is still too high”, adding that “risks to inflation are judged to be skewed to the upside.” But the guidance was tempered at the margin with the Board now prepared to “increasing the cash rate further if upside risks [to inflation] materialise”, rather than simply “if needed” previously."

"Indeed, the RBA’s updated forecasts raised the bar for another hike. The RBA raised its unemployment rate projection across the forecast horizon and lowered its policy-relevant trimmed mean inflation projections through June 2027."

"AUD/USD dipped briefly following the policy decision but recovered most of the losses during RBA Governor Michele Bullock’s press conference. Bullock highlighted it was “quite possible” that a further rate hike would be needed, pointing out that Australia’s economy is still operating above capacity."

"Bottom line, attractive carry alongside Australia’s strategic exposure to commodities linked to energy, AI, and defense remain key AUD tailwinds."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

- Silver loses more than 2% on Tuesday after hitting a seven-week high on Monday.

- Rising Oil prices revive inflation concerns and strengthen expectations of higher interest rates.

- Negotiations surrounding the Strait of Hormuz and US inflation data remain in focus.

Silver (XAG/USD) extends its correction on Tuesday and trades around $65.05 at the time of writing, down 2.31% on the day. The white metal retreats from the seven-week high reached at $66.59 on Monday as rising Oil prices and prospects of tighter monetary policy in the United States (US) weigh on precious metals.

Oil prices have risen sharply since the beginning of the week as negotiations aimed at reopening the Strait of Hormuz remain uncertain. Iran is conditioning the reopening of this strategic maritime route on several demands from Washington, including the payment of war reparations and the lifting of sanctions.

Some signs of easing tensions are nevertheless emerging. Qatar says on Tuesday that negotiations between Oman and Iran have reached an advanced stage and that it has received positive feedback from both sides. Doha stresses, however, that the talks are at a critical juncture, maintaining uncertainty over the prospect of a swift agreement.

This situation supports energy prices and revives concerns about US inflation. West Texas Intermediate (WTI) trades around $81.20, up more than 5% since the beginning of the week, despite the daily decline. Higher Oil prices are also helping to keep US Treasury yields elevated, reducing the appeal of Silver, a non-yielding asset.

Against this backdrop, investors are increasing their expectations of further monetary tightening by the Federal Reserve (Fed). According to the CME FedWatch tool, markets now estimate a 52% chance of a 25-basis-point interest rate hike at the September meeting, up from approximately 44% the day before.

Comments from Cleveland Federal Reserve (Fed) President Beth Hammack are also fueling these expectations. Hammack said on Monday that current monetary policy “is not hurting the economy” and argued that the Fed will need to raise interest rates more than once to bring inflation back toward its target.

These prospects provide some support to the US Dollar (USD) and represent an additional headwind for Silver. A stronger US Dollar tends to make the white metal more expensive for investors using other currencies, while higher interest rates increase the opportunity cost of holding non-yielding assets.

Investors now turn their attention to the US Consumer Price Index (CPI) data due on Wednesday. Stronger-than-expected inflation could reinforce expectations of a September rate hike and maintain pressure on Silver. Conversely, easing price pressures could reduce expectations of monetary tightening and provide support to the precious metal.

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

OCBC’s Sim Moh Siong and Christopher Wong note the US Dollar (USD) softened as Fed hike expectations moderated and the US yield curve steepened. They argue that without a strong upside surprise in United States (US) Consumer Price Index (CPI), the USD should stay rangebound, supporting carry trades. Debasement concerns and scrutiny of Fed independence are seen underpinning Gold, while upcoming US CPI, PPI and retail sales will steer Fed expectations.

Dollar tied to upcoming CPI data

"The USD softened over the past week as Fed rate hike expectations moderated and the US yield curve steepened. Unless this week's CPI report delivers a meaningful upside surprise, the USD is likely to remain trapped in narrow ranges. July's soft payrolls report should keep the Fed patient beyond September, with markets unlikely to price a September hike as the base case without a firmer inflation signal."

"In our view, core CPI would need to print at 0.3% MoM or higher in July, above the 0.2% consensus forecast, to materially lift expectations of a September rate hike. A rangebound USD, combined with a constructive risk backdrop, should continue to support carry trades despite ongoing volatility in oil markets. Oil prices eased on hopes that the Strait of Hormuz could reopen, but Iran's firm conditions for Washington suggest any near-term boost to energy supply is likely to be limited."

"Meanwhile, debasement concerns have returned to the fore, adding pressure on the USD and helping gold rebound from what increasingly appears to be a floor near USD4,000/oz. Several recent developments have renewed scrutiny over Fed independence."

"First, the Trump administration reportedly made another attempt to remove Fed Governor Lisa Cook. If successful, President Trump would gain an additional opportunity to appoint a Fed governor. Cook has until 26 August to respond. Second, the Wall Street Journal reported that President Trump has maintained frequent contact with Fed Chair Kevin Warsh, discussing issues ranging from Iran to AI. While there is no evidence that monetary policy has been directly influenced, the relationship appears less distant than the convention typically observed between the White House and the Fed."

"Following the weak July payrolls data, we do not believe a Fed decision to keep rates unchanged in September would be viewed as a credibility issue. However, if inflation remains sticky, the September meeting could become an important test of the Fed's inflation-fighting credentials. In that scenario, the USD outlook will depend heavily on whether policymakers choose to reinforce their inflation mandate through tighter policy."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)

- USD/CHF consolidates above 0.8100 after bouncing from Friday's lows near 0.8050.

- The US Dollar is drawing support from the uncertain US-Iran peace process and hawkish Fed speak.

- FX volatility remains below average, with investors awaiting Wednesday's US CPI report.

The Swiss Franc trades practically flat against the US Dollar (USD) on Tuesday, consolidating halfway through last week’s trading range. The USD/CHF pair bounced up from Friday’s lows just above 0.8050 on Monday, amid growing concerns about the fate of the US-Iran peace negotiations and hawkish comments from Federal Reserve (Fed) officials, with FX volatility subdued ahead of the US Consumer Price Index (CPI) release, due on Wednesday.

In the absence of key macroeconomic releases on Tuesday, developments in the Middle East are driving markets with growing uncertainty about the peace plan pushing Oil prices higher and curbing investors’ appetite for risk. US and Iran fail to find a formula to reopen the Strait of Hormuz, entangled in reciprocal requests for war damage compensation, and drifting away expectations of a swift resolution of the conflict.

Beyond that, Cleveland Federal Reserve (Fed) President Beth Hammack affirmed on Monday that the central bank might have to hike interest rates more than once to bring inflation to target. This has fuelled hopes of some monetary tightening in September, offsetting the negative impact from Friday's US Nonfarm Payrolls, and providing some support to the US Dollar.

OCBC: USD seen rangebound as Fed hike bar stays high

Regarding US consumer inflation, strategists at OCBC argue that Wednesday's report would need to deliver a clear upside surprise to meaningfully shift the policy narrative. In their view, "core CPI would need to print at 0.3% MoM or higher in July, above the 0.2% consensus forecast, to materially lift expectations of a September rate hike."

Against this backdrop, they expect that "a rangebound USD, combined with a constructive risk backdrop, should continue to support carry trades despite ongoing volatility in oil markets." Nevertheless, they warn that "Iran's firm conditions for Washington suggest any near-term boost to energy supply is likely to be limited."

The Swissie, however, is unlikely to perform any significant recovery, according to OCBC experts, "as carry trade funding demand grows and the SNB appears comfortable with a weaker currency.” With “inflation subdued and policy rates likely anchored at zero, CHF weakness could persist into year-end,” said OCBC analysts in a note.

Swiss Franc FAQs

The Swiss Franc (CHF) is Switzerland’s official currency. It is among the top ten most traded currencies globally, reaching volumes that well exceed the size of the Swiss economy. Its value is determined by the broad market sentiment, the country’s economic health or action taken by the Swiss National Bank (SNB), among other factors. Between 2011 and 2015, the Swiss Franc was pegged to the Euro (EUR). The peg was abruptly removed, resulting in a more than 20% increase in the Franc’s value, causing a turmoil in markets. Even though the peg isn’t in force anymore, CHF fortunes tend to be highly correlated with the Euro ones due to the high dependency of the Swiss economy on the neighboring Eurozone.

The Swiss Franc (CHF) is considered a safe-haven asset, or a currency that investors tend to buy in times of market stress. This is due to the perceived status of Switzerland in the world: a stable economy, a strong export sector, big central bank reserves or a longstanding political stance towards neutrality in global conflicts make the country’s currency a good choice for investors fleeing from risks. Turbulent times are likely to strengthen CHF value against other currencies that are seen as more risky to invest in.

The Swiss National Bank (SNB) meets four times a year – once every quarter, less than other major central banks – to decide on monetary policy. The bank aims for an annual inflation rate of less than 2%. When inflation is above target or forecasted to be above target in the foreseeable future, the bank will attempt to tame price growth by raising its policy rate. Higher interest rates are generally positive for the Swiss Franc (CHF) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken CHF.

Macroeconomic data releases in Switzerland are key to assessing the state of the economy and can impact the Swiss Franc’s (CHF) valuation. The Swiss economy is broadly stable, but any sudden change in economic growth, inflation, current account or the central bank’s currency reserves have the potential to trigger moves in CHF. Generally, high economic growth, low unemployment and high confidence are good for CHF. Conversely, if economic data points to weakening momentum, CHF is likely to depreciate.

As a small and open economy, Switzerland is heavily dependent on the health of the neighboring Eurozone economies. The broader European Union is Switzerland’s main economic partner and a key political ally, so macroeconomic and monetary policy stability in the Eurozone is essential for Switzerland and, thus, for the Swiss Franc (CHF). With such dependency, some models suggest that the correlation between the fortunes of the Euro (EUR) and the CHF is more than 90%, or close to perfect.

- GBP/USD ticks lower to near 1.3500 as the US Dollar edges up.

- Traders have trimmed hawkish Fed bets after weak US NFP data for July.

- Investors await the US CPI and the UK GDP data.

The GBP/USD pair trades marginally lower at around 1.3500 during the European trading session on Tuesday. The Cable edges down as the US Dollar (USD) ticks up; however, financial markets doubt the slight recovery move seen this week, with traders paring hawkish Federal Reserve (Fed) bets for the September policy meeting due to weak United States (US) Nonfarm Payrolls (NFP) data for July.

US payrolls stumble as July jobs data disappoints

Economists at ING describe the July US jobs report as "surprisingly weak," noting that nonfarm payrolls "fell 23k" on the month. They highlight that the softness was compounded by "103K of downward revisions to the past two months' data," which has dragged the "3M average" gain in payrolls down to just "20,000." ING argues that this combination of an outright monthly decline and sizeable revisions paints a notably softer picture of underlying labour market momentum.

According to the CME FedWatch tool, the odds of the Fed holding interest rates steady in the September meeting have increased to 50% from 30.4% seen a month ago.

Going forward, investors will focus on the US Consumer Price Index (CPI) data for July and the United Kingdom (UK) Q2 and June Gross Domestic Product (GDP) data, which will be released on Wednesday and Thursday, respectively.

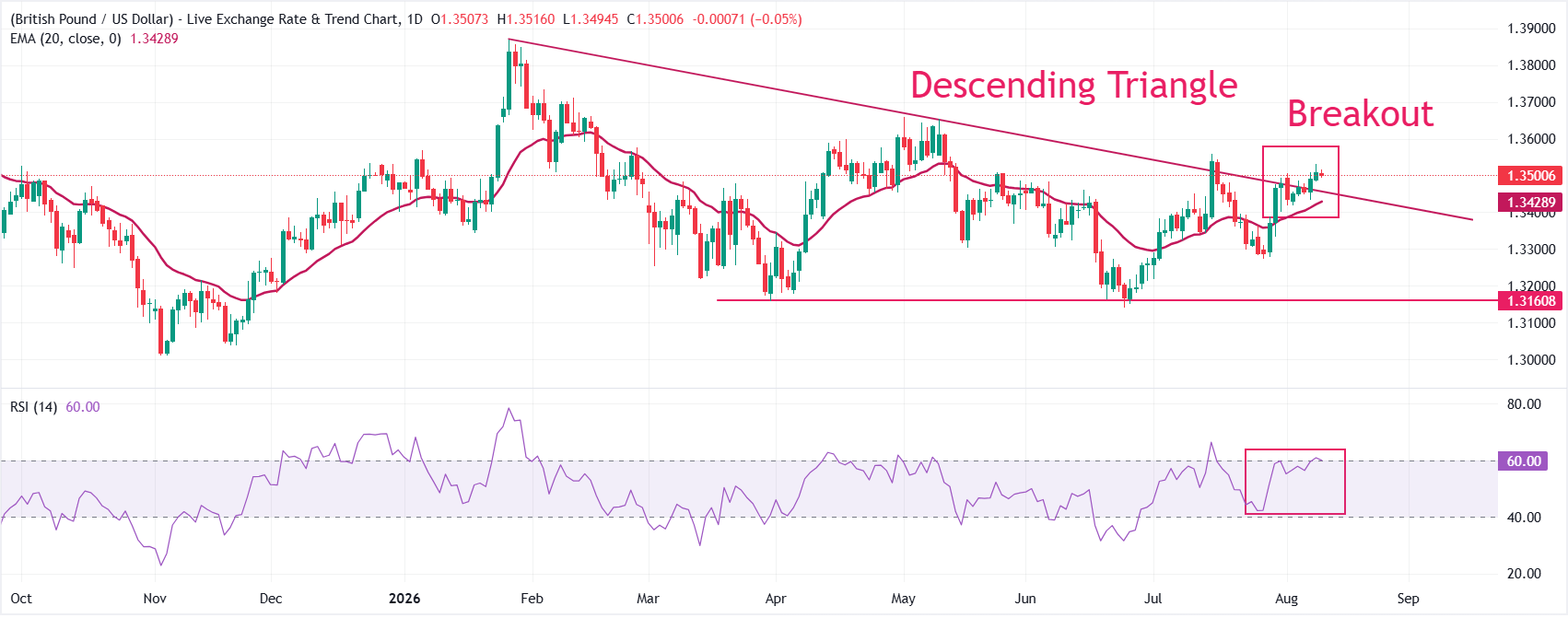

GBP/USD Technical Analysis

GBP/USD trades around 1.3501, holding a bullish near‑term bias as spot remains above the 20-period exponential moving average (EMA) at 1.3429 and the downward-sloping border of the Descending Triangle pattern offering support near 1.3455.

The pair is thus supported by both dynamic and structural levels, while the Relative Strength Index (14) at about 60 points to firm but not overextended bullish momentum, suggesting buyers still control the near-term direction.

On the downside, initial support is seen at the former resistance trend line turned floor around 1.3455, followed by the 20-period EMA at 1.3429, where dip buyers may re-emerge if corrective pressure unfolds. Looking up, the pair could advance towards 1.3600 if it manages to extend the advance sustainably above the July 15 high at 1.3558.

(The technical analysis of this story was written with the help of an AI tool. Know more.)

Economic Indicator

Consumer Price Index (YoY)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The YoY reading compares the prices of goods in the reference month to the same month a year earlier.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Wed Aug 12, 2026 12:30

Frequency: Monthly

Consensus: 3.4%

Previous: 3.5%

Source: US Bureau of Labor Statistics

The US Federal Reserve (Fed) has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

Talks between Oman and Iran have reached an advanced stage, Qatar’s Foreign Ministry spokesperson said on Tuesday.

Speaking at a press conference, Majed al-Ansari said the negotiations were at a “critical juncture” and stressed that Doha supports all efforts to ease tensions in the region.

“As mediators, we want the Strait of Hormuz reopened as soon as possible,” al-Ansari said.

Qatar said it has received positive feedback from both Oman and Iran and supports any arrangement that guarantees the security of the Strait of Hormuz and freedom of navigation.

Market reaction

West Texas Intermediate (WTI) Oil fell sharply from an intraday high of $83.57 following the comments. At the time of writing, WTI trades around $81, while holding most of Monday’s 6.66% gain.

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 12 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

ING strategists Warren Patterson and Ewa Manthey report that European Natural gas benchmark TTF jumped over 9%, moving back above EUR60/MWh as hopes for a US–Iran deal fade. They warn that each day without Persian Gulf LNG flows and falling European storage levels, now below 2021 benchmarks, increases vulnerability to price spikes during the 2026/27 heating season.

Storage worries into 2026/27 heating season

"Fading optimism over a potential deal between the US and Iran has also seen European natural gas prices surge higher once again."

"TTF settled more than 9% higher yesterday, taking it back above EUR60/MWh."

"Every day that goes by without a resumption of Persian Gulf LNG flows leaves the market more vulnerable as we head closer towards the 2026/27 heating season."

"Gas storage is now below 2021 levels both in terms of percentage full and in absolute terms."

"The EU’s lower storage target of 75% ahead of the winter is looking as though it will be tough to hit."

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.)